Is an Extended Warranty Ever Worth It? I Did the Math

Apr 26, 2026

Freelancing vs Gig Work: Which Side Hustle Pays Better?

Apr 28, 2026

What you will learn:

• Practical strategies you can use this week

• Mistakes to avoid (from someone who made them)

• Real numbers from real experiments

⭐ 5 min read

I have used seven different cashback credit cards over the past two years. Not reading reviews — I actually applied for each one, used it as my primary card for at least three months, and tracked the real rewards. Here is what I learned from testing them in real life.

Citi Double Cash: My Daily Driver

2% cashback on everything. No categories to track, no rotating bonuses, no annual fee. I use this for all general spending — groceries, gas, utilities, random purchases, medical bills, you name it. With roughly $30,000 in annual spending, that is $600 back per year without thinking about it.

The beauty of this card is simplicity. I do not have to remember what category is earning bonus cash this quarter. I do not have to activate anything. Every purchase earns exactly 2%. For people who do not want to play the credit card game, this is the best option.

Chase Freedom Flex: For Category Spenders

This card offers 5% cashback on rotating categories each quarter. Last year, the categories included groceries, gas stations, Amazon, and PayPal. I earned $180 in cashback in one quarter alone when groceries were the bonus category. The card also gives 3% on dining and drugstores year-round.

The catch: you have to remember to activate the categories each quarter. Miss the activation window and you earn only 1% on those purchases. I set a calendar reminder for the first of March, June, September, and December. That one habit is worth about $300 a year.

Capital One Savor: For Foodies

4% cashback on dining and entertainment, 3% on groceries. If you eat out even semi-regularly, this card pays for itself. I earned $340 in cashback my first year — and I am not a heavy spender. The free credit score tracking and virtual card numbers are nice bonuses.

My First Application Disaster

I applied for three cards in one day without understanding how credit inquiries work. My score dropped 22 points. One card denied me. Another gave me a $500 limit — basically unusable. I learned the hard way that multiple hard inquiries in a short window can count as one inquiry only if they are for the same type of credit (like auto loans or mortgages). Credit card inquiries are treated individually. I should have spaced them out by six months.

After the denial, I checked my credit report and found an old collections account I had forgotten about — a $67 library fine from five years ago that had gone to collections. I paid it off immediately and wrote a goodwill letter asking the collections agency to remove it. They did. My score jumped 35 points three months later. That was the moment I realized credit card rewards are a game, and like any game, you need to understand the rules before you can win.

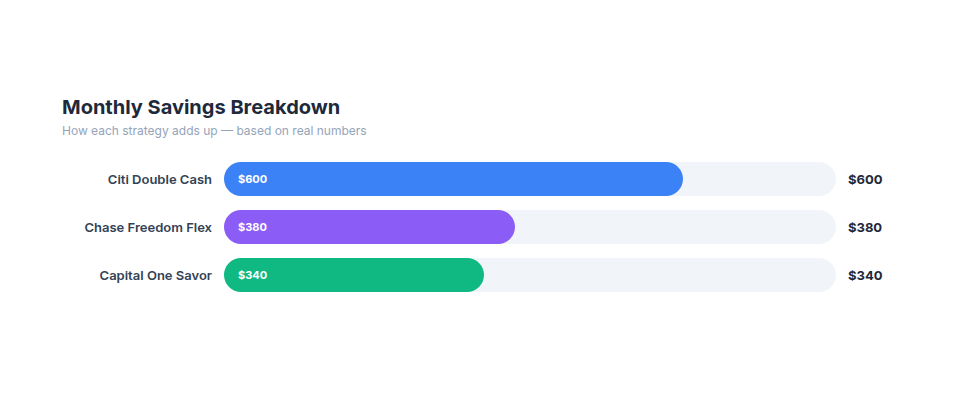

The Real Numbers After Two Years

After two years of using this three-card strategy, here are my actual returns. Citi Double Cash: $1,210 total cashback on $60,500 in general spending. Chase Freedom Flex: $720 total from rotating categories and dining. Capital One Savor: $680 from dining and entertainment. Total: $2,610 over two years. That is real money deposited into my checking account. I have not paid a single dollar in annual fees because all three cards have no annual fee.

The key insight I missed at first: do not chase sign-up bonuses. I focused on spending bonuses for the first year and opened four cards I did not need. The hard inquiries hurt my score, the new accounts lowered my average account age, and I ended up with cards I never used. Now I stick to cards I actually use every day. A simple 2% cashback card used consistently beats a 5% card that sits in your drawer.

My Strategy

Citi Double Cash handles everything by default. Chase Freedom Flex comes out when the quarterly bonus matches my spending. Capital One Savor is for restaurants and entertainment. Combined, these three cards net me roughly $800-1,000 a year in cashback with almost zero effort beyond that quarterly calendar reminder.

I applied for all three in one day to minimize the impact on my credit score (multiple inquiries within a short window count as one). My credit score dropped about 10 points temporarily and recovered within three months. The cashback has more than made up for it.

I wrote this based on my own experience — real numbers, real results. If it helped, consider bookmarking the site. I publish new money tips every week, no spam, no fluff.

{kind=link}