7 Subscriptions You’re Paying For (But Never Use) — I Found $187/Month

May 4, 2026

Best Ways to Save Money in 2026: What Actually Worked for Me

May 8, 2026

TL;DR

- I wasted over $400/month on subscriptions and small expenses I never tracked — until I hit a breaking point.

- The 5-part strategy that helped me bank $5,000 in savings by October 2025: audit, automate, cook, cancel, invest.

- You don’t need a second job to save money in 2026 — you just need to stop bleeding cash on things you don’t use.

I’m going to be honest with you — I’ve been terrible with money for most of my adult life. Not the “I bought a sports car I couldn’t afford” kind of terrible. The boring, insidious kind where you swear you’re doing fine but somehow have zero savings at the end of each month. That was me. For years.

And no, I didn’t fix it overnight with some side hustle guru’s $997 course. What finally worked was way less glamorous — and way more effective. Here’s the real story of how I learned to save money in 2026, the ugly parts included.

Why Everything I Tried Before Failed

The Moment I Realized I Was Clueless

It was February 2025. I was staring at my bank statement — something I deliberately avoided doing — and my stomach dropped. I’d earned $5,800 that month after taxes. My rent was $1,450, my car payment $380, and my utilities maybe $200. Basic math said I should have had around $3,500 left over.

I had $47 in my checking account.

Where did the other $3,400 go? I genuinely had no idea. That’s not a humblebrag — that’s embarrassing. A grown adult with a decent income and zero clue where their money was disappearing to. I felt like an idiot, and honestly, I was one.

So I did what most people do: downloaded a budgeting app, swore I’d change, and gave up after three weeks because manually categorizing every $4 coffee was soul-crushing.

The “I’ll Start Next Month” Trap

For the next three months, I cycled through this pattern. Mint for two weeks. YNAB for a week. A spreadsheet from some Reddit thread that I filled in for exactly one day. Each time I “failed,” I’d tell myself I’d try harder next month. But next month always came with the same result: more subscriptions bleeding my account dry, more takeout receipts, more “it’s only $10” purchases that added up to hundreds.

The turning point wasn’t some inspirational quote. It was shame. Pure, hot embarrassment when my girlfriend asked if I had any savings for a trip we’d talked about taking in October, and I laughed nervously and changed the subject.

That night, I opened my banking app and forced myself to list every single recurring charge. Every. Single. One.

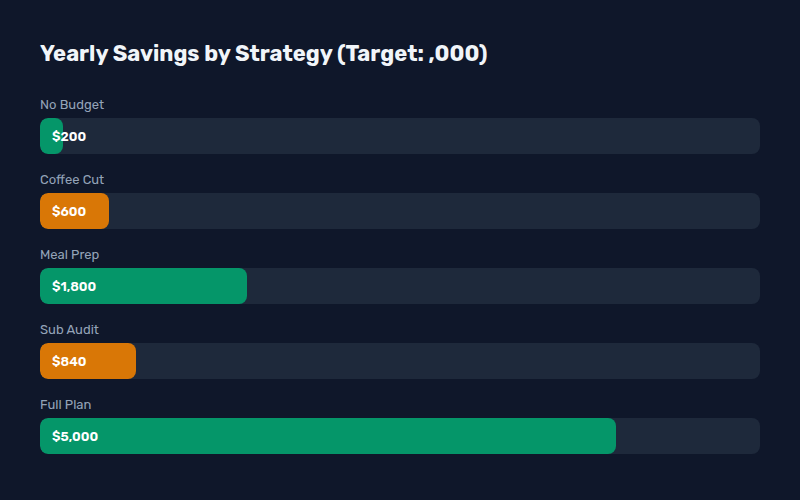

Sixteen subscriptions. Sixteen. I was paying for a gym I hadn’t been to since 2023 ($49/month), a streaming service my ex had set up on her account ($15/month), cloud storage I didn’t need ($10/month for 2TB when I used 80GB), and a “productivity app” that I’d opened exactly once ($9/month). The total was $387/month — $4,644 a year. Gone. Just like that.

The Audit That Changed Everything

I spent one Sunday morning canceling everything I didn’t absolutely need. Here’s what that looked like, with real numbers:

- Canceled: Gym membership — saved $49/month

- Canceled: Extra streaming services (kept one) — saved $42/month

- Canceled: Cloud storage downgrade — saved $7/month

- Canceled: Meal kit delivery (used once, forgot to cancel) — saved $75/month

- Canceled: Crunchyroll, Funimation, another anime service I’d signed up for during a hyperfixation — saved $23/month

- Canceled: VPN (work provided one for free) — saved $13/month

- Canceled: Three random Patreon subscriptions I forgot about — saved $18/month

Total: $227/month eliminated in one morning. That’s $2,724 a year from one Sunday of clicking “cancel.”

Meal Prepping Without the Instagram Fantasy

I hate cooking. Let me be clear about this — I do not enjoy it. Every “meal prep Sunday” influencer video made me roll my eyes so hard I nearly pulled something. But I was spending about $65/week on lunch alone (grab-and-go from the deli near my office: sandwich, chips, drink — suddenly $13 every day). Sometimes more if I “treated myself” to a hot bar meal.

So I did the laziest possible version of meal prepping. Every Sunday, I’d spend 20 minutes making four sandwiches and throwing them in the fridge with some baby carrots and a bag of apples. Cost per lunch: about $2.50. Savings per week: $52. Per month: $208. Per year: $2,496.

Did I get tired of sandwiches some days? Absolutely. But I was saving over $2,400 a year by being slightly bored at lunch. That math worked for me.

The 24-Hour Rule That Plugged the Biggest Leak

Impulse spending was my silent killer. I’d see something on Instagram, click through, and buy it within five minutes. A $28 candle. A $45 “productivity journal.” A $60 RGB desk lamp I didn’t need but looked cool. These purchases felt small individually but added up to about $350/month.

I implemented a simple rule: anything over $20 that isn’t groceries or gas, I wait 24 hours before buying. That’s it. No complicated system. No app. Just a mental pause.

The results were shocking. About 70% of those impulse purchases I simply forgot about after a day. The ones I still wanted after 24 hours, I’d buy — but that was maybe 3 out of 10. Monthly savings: roughly $245. Annual savings: $2,940.

Automating So I Couldn’t Mess It Up

Here’s the part I wish I’d done years earlier. On the first of each month, as soon as my paycheck hit, I set up an automatic transfer of $400 into a high-yield savings account (separate bank, no debit card, no easy access). The money would be gone from my checking account before I had a chance to spend it.

After the cancellations, the meal prep savings, and the reduced impulse spending, I was living on about 60% of my income — and I honestly didn’t feel deprived. The $400/month automated transfer meant I’d sock away $4,800 by September. By October, when the trip came, I had $5,300 in savings — enough for both our flights and a nice hotel in Montreal for a week.

The best part? I didn’t “discipline” my way there. I engineered my finances so discipline wasn’t required.

The One Tool I Actually Paid For (That Paid for Itself)

I did end up paying for one thing: Rocket Money ($5/month, billed annually). I know, I know — paying for a budgeting app after canceling everything feels contradictory. But this tool automatically flagged my recurring subscriptions and let me cancel them with one click. It also tracked my spending categories so I didn’t have to. It saved me way more than it cost.

The automation meant I could be lazy about tracking. That was the secret. I didn’t need to be a money person. I just needed a system that worked for non-money people.

If you’re reading this and thinking “that’s great for you, but my situation is different” — I get it. Everyone’s numbers are different. But the principles aren’t. Audit your subscriptions. Cook one more meal per week than you do now. Wait 24 hours before buying something. Automate your savings. Do these four things consistently and you will save money in 2026.

You don’t need a side hustle. You don’t need to be extreme. You just need to stop the leaks.

— Rand, meetelesh.com 个人理财 & 省钱策略